501(c)(8) is an Internal Revenue Service (IRS) tax exemption status that applies to "fraternal beneficiary societies, orders, or associations operating under the lodge system...and providing for the payment of life, sick, accident, or other benefits to the members of such society, order, or association, or their dependents."

I’m tipping a golden calf. But imagine a future in which you join a mutual society instead of a political party to provide for your healthcare and retirement. Instead of Team Red and Team Blue competing for votes to gain power and make a monolithic system for 330 million people, a thousand benefit associations would bloom to replace Social Security, Medicaid, and Medicare after those damnable programs’ repeal.

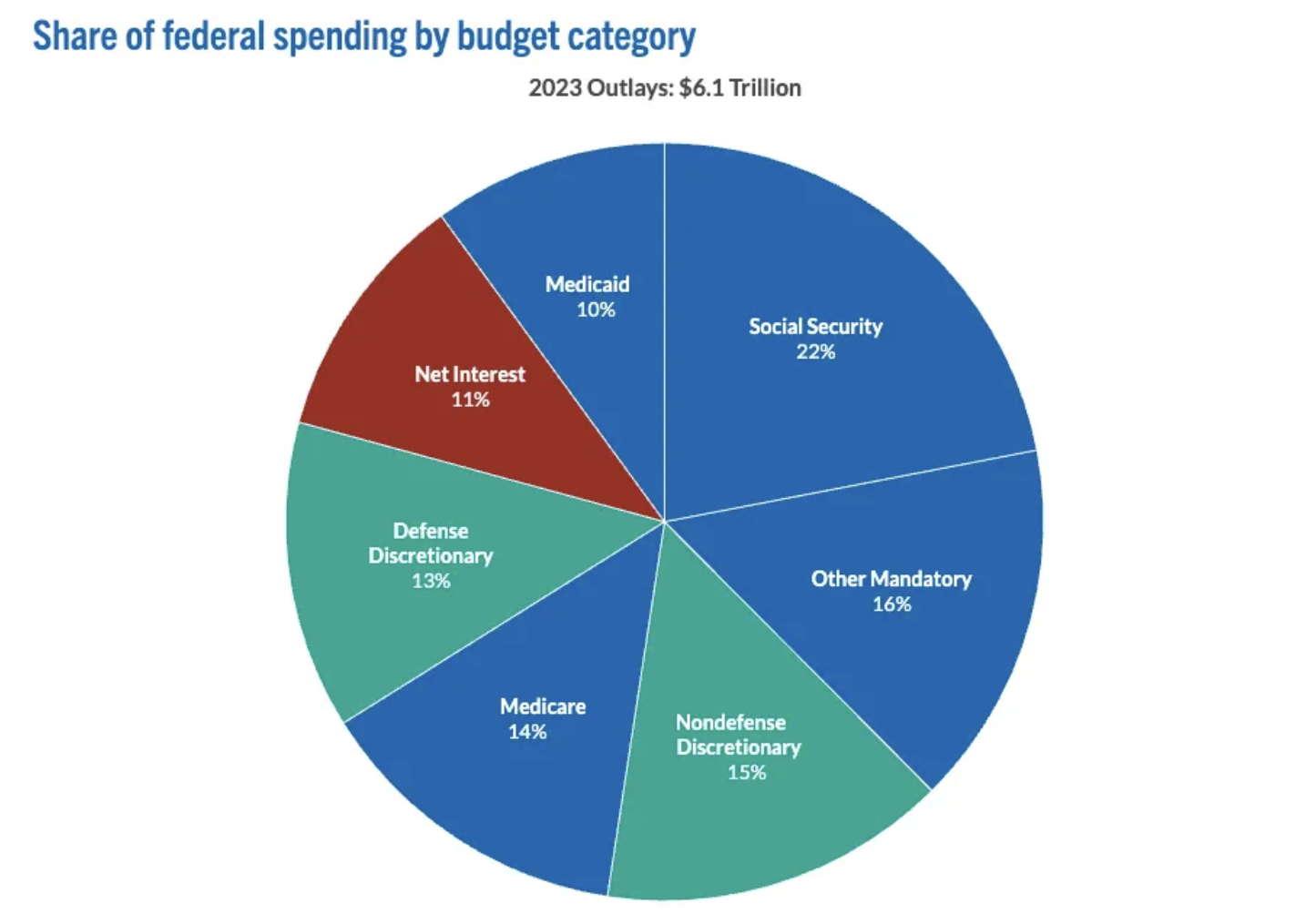

Let’s take three of the four systems listed in blue below: Medicaid, Social Security, and Medicare, which comprise 46 percent of the federal budget. That’s $2.8 trillion in taxpayer dollars.

Now imagine that $2.8 trillion were spent differently. Assume that anyone who makes under $500,000 per year was required by law to join an association in lieu of paying for entitlements, with correspondingly lower taxes. Anyone in the top 1 percent of earners would be encouraged to participate, though perhaps as charitable stewards. I don’t like forced association, but we’re granting it as a replacement for, at least, FICA taxes.

That same group (the “99 percent”) pays about $4,000 annually in FICA taxes on average for the employee contribution. Would that suffice? Given so many diverse circumstances, this isn't easy to calculate, but we can scrawl it on the back of an envelope.

- Assume 237.7 million Americans in the “99 percent” are required to join, similar to how drivers are mandated to carry car insurance.

- Assume that each pays (on average) what is currently required in FICA taxes ($4,000).

- The result? About $1 trillion, or less than half (46 percent) of total entitlement spending.

So, between the per American cost of entitlements—$8,235.29 ($18,667 per beneficiary)—and the $4,000 the 99 percent spends on FICA taxes, would benefit associations be able to do better than the Big Three Entitlements?

Maybe. But let’s stipulate that it’s insufficient.

Assume now that the average working person would have to pay $6,000 per year, on average, or $500/month, to a mutual society instead of FICA plus $2,000 in income taxes. Such amounts to $1.5 trillion in dedicated benefit association dollars. We would need an additional $1.3 trillion in system savings to match the aggregate spending of the former system. I’ll return to this later.

Who knows? Maybe one would look something like the following:

- The Society of Virtue

- $6,000 per year or $550 per month, flat fee

- Lowest income decile free membership (limited spots)

- Health plan, Unemployment, Retirement

- 4 out of 5 stars

- Requires abstaining from tobacco, drugs, and alcohol

- Progressive Alliance

- $100 per month to $800 per month, sliding income scale

- Health plan, Unemployment, Retirement

- Basic Income Assistance for those in the lowest quintile

- 3.5 out of 5 stars

- Pledge requirement

- Free Builders

- Percentage of income, sliding income scale

- Health plan, Mutual aid

- Legal Assistance

- 4.5 out of 5 stars

- Minimum two-year signup

- Basic Income Alliance

- 10% of income

- Health plan, Unemployment, Retirement

- Basic Income guarantee on a sliding scale, according to income

- 4.1 out of 5 stars

- 2-year Minimum Membership

- Friends of Hillel

- $6,000 per year

- Lowest income quintile free membership (limited spots)

- Health plan, Mutual Aid

- 4.7 out of 5 stars

- Jewish institution, but being Jewish not required

- St. Mary's Society

- Percentage of income on sliding scale

- Health plan, Mutual Aid, Unemployment

- Lowest income quintile free membership (limited spots)

- 4.4 out of 5 stars

- Catholic Requirement

- Conservatives United

- Percentage of income on sliding scale

- Health plan, Mutual Aid, Legal Assistance, Unemployment

- 4.8 out of 5 stars

- Pledge requirement

- Order of the Leaf

- Health plan, Mutual Aid, Unemployment

- Lowest income quintile free membership (limited spots)

- 4.5 out of 5 stars

- Veganism dietary requirement

- Union of Working People

- $200-$650 per month, tiered

- Health plan, Mutual Aid, Unemployment

- Basic Income Assistance

- 4.7 out of 5 stars

- Pledge and work requirement

- The Freethinkers

- $400/month

- General Mutual Aid

- Lowest income decile free membership (limited spots)

- Able-bodied retiree volunteer requirement

- 4.8 out of 5 stars

- Atheism requirement, Pledge requirement

- Peace Communists

- Fee tiers based on income

- Basic Income Guarantee

- Lowest income quartile, free membership, limited spots

- Pledge Requirement

- 2.8 out of 5 stars

- Two-year minimum commitment

We can imagine these benefit associations having unique content, programming, and opportunities for more intimate member interaction that one can expect from the IRS or HHS. Still, I made them up.

What would social entrepreneurs dream up?

Feasibility

Consider that in the heyday of mutual aid associations before the New Deal, members paid only about 2 percent of their incomes for a full suite of benefits. We can’t expect 2 percent to scale through time, especially given inflation. Still,

- Life Insurance. Members received financial support for their families in the event of death.

- Sickness and Disability Benefits. Financial assistance was provided during illness or disability, ensuring members could maintain their livelihoods.

- Medical Care. Some societies operated their own clinics or hospitals, offering medical services to members at little or no additional cost.

- Funeral and Burial Services. Societies often covered funeral expenses and provided burial plots, alleviating financial burdens during times of loss.

- Support for Widows and Orphans. Assistance was extended to the families of deceased members, including financial support and education for children.

- Social and Educational Activities. Beyond financial benefits, these organizations fostered community through social events, educational programs, and cultural activities.

Of course, people will prioritize different things today. Our standard of living is higher, and we demand more expensive services.

Now, some might be skeptical that these associations would work at my average cost point. Perhaps they’re right. But consider some facts that make this great replacement far more plausible:

- Consider that the people of the United States spend 18 percent of GDP on health care. By contrast, Singapore spends less than 5 percent and achieves better health outcomes. This indicates that as much as 13 percent of US GDP could be in bloat. (15% of US GDP = $4.5 trillion) If we abandoned our current entitlement and healthcare systems and adopted a competitive mutual aid model plus a patient-centric (price-competitive) healthcare system like Singapore’s, we could reasonably save at least $1 trillion.

- With a mutual model, members have incentives to curb cost-shifting and third-party payer effects. So, the likeliest scenario regarding healthcare is that the mutual societies would only cover catastrophic care and leave routine and out-of-pocket expenses to members’ large pre-tax health savings accounts. (Remember also that the mutuals of old required 2% of income.)

- With retirement benefits, I asked AI to help me calculate what the average American would expect if he or she contributed just half of what she contributed over her 40-year career into Social Security into the S&P 500, assuming she retired today. Here is the result: “If the average American redirected half of their Social Security contributions (6.2% of earnings) to the S&P 500 over a 40-year career, they might have approximately $650,000–$700,000 in total assets today, May 30, 2025. In contrast, the average Social Security benefit provides $23,712 annually, with a lifetime value of $474,240 without COLA adjustments, or potentially $600,000–$700,000 with inflation adjustments over 20 years.”

- If the average American earns $200,000 in nominal Social Security contributions via paychecks over a 40-year career (1985 to 2024) and redirects those funds to pay mutual society dues out of each paycheck—where dues are equivalent to $500 per month in 2025 dollars (adjusted backward for 2.5% inflation, e.g., $186.22 in 1985)—she can afford:

- 40 years of membership during her career (1985 to 2024), fully covered by the redirected contributions.

- Approximately 8.4 years after 2024, using the remaining $49,385.

- Total: Approximately 48.4 years of membership. That means if she were to run out of (what would have been) her equivalent social security contribution at 73.4 years, then the aid association would likely only have to waive her membership dues in retirement for 6.6 years, on average (assuming she lives to 80). Such assumes she has no other savings.

- The average American conservatively contributes ~$450 per month to a defined-contribution plan (employee + employer).

- With $450 monthly, growing at 2.5%, invested at a conservative 7% nominal return, the plan grows to ~$1.47 million after 40 years.

- Adding $6,000 per year ($500/month) for the mutual society, the total annual commitment starts at $11,400 in 1985 and grows to ~$30,692 by 2024. Over 40 years, the average worker contributes $768,400, yielding $404,400 spent on the association and ~$1.47 million in savings, or ~$1.88 million in total resources by 2025.

Suppose this sort of benefit association replaced entitlements in the future. In that case, some would want to know how most people would be able to oblige non-members to pay their 'fair share' or otherwise live by their conception of the good. Beyond the power of persuasion, they won't. The whole point of membership is that a moral-political community shares similar commitments, and the value of membership binds them to a particular association.

If a mutual society can help its members thrive sustainably, it will gain more members. If one believes there is some objective percentage of income one should set aside to help others, she will have to find others who feel the same. Otherwise, those outside her community may have different commitments and wish to belong to another benefit association. But at least no benefit association can permanently bind anyone to its rules. Everyone has a choice.

Some will not be comfortable with this idea.

But remember, the mutual aid era was killed less than one-hundred years ago.

- 1935. Congress passed the Social Security Act, introducing federal old-age benefits and unemployment insurance. This marked a significant shift in responsibility from voluntary associations to the state.

- 1940s. The expansion of employer-based health insurance during World War II (driven by wage controls) began to crowd out the need for mutual aid healthcare services.

- 1960s. Continued growth in welfare programs, including Medicare and Medicaid, further diminished the functional necessity of mutual aid societies.

The federal government killed an empire of benevolence.

The federal government could resurrect it, too, though the specter of sovereign default might be the only force to goad its proxies. As Milton Friedman once said,

The way you solve things is by making it politically profitable for the wrong people to do the right thing.

Sadly, a majority of Americans think that our big, bloated welfare state monopoly is more or less the apotheosis of the general welfare. But that seems like an odd opinion due to the fiscal cliff we’re currently staring down.

Pluralism, Please

Just as people in Texas cannot require those living in Thailand, Tahiti, or Tijuana to conform to Texas laws or norms, no one could force you to join a particular mutual society. Why should the history of conquest over great expanses of soil bind everyone to the same shitty systems, or to some monopoly taxation and debt regime? In this condition, the only questions anyone needs to worry about are whether or not their benefit association delivers on its commitments to members and remains solvent.

But why shouldn’t there be a single conception of social justice and thus one system for everyone? Why can’t there be a philosopher king who has absolute knowledge of the right and the good?

As biologist E.O. Wilson says, “Like everyone else, philosophers measure their personal emotional responses to various alternatives as though consulting a hidden oracle.” He continues:

That oracle resides in the deep emotional centers of the brain, most probably within the limbic system, a complex array of neurons and hormone-secreting cells located just beneath the "thinking" portion of the cerebral cortex. Human emotional responses and the more general ethical practices based on them have been programmed to a substantial degree by natural selection over thousands of generations.

There is wild variation because our hidden oracles rarely say the same things. Our ethical practices will be diverse, too.

Some might argue that pluralism is relativism, but I think not. Instead, it acknowledges our different values, proclivities, circumstances, and needs. Instead of forcing everyone to participate in the same system, we allow an array of systems to be organized according to the facts and values of pluralism. Factual, because we’re undoubtedly different and live in diverse circumstances. Such facts prompt us to value different communities, systems, and associations.

What binds us together, then, is pluralism.

One of the benefits of panarchy—radical association—is that it dismantles any central levers of authority over which partisans fight. In this way, it dismantles monopolistic claims to moral authority. Finally, we agree that politics is a perverse, cyclical tug-of-war that locks the people in conflict. The two American political parties have formed a cartel of bitter rivalry, but a cartel nonetheless. The only thing they agree about is that war is good for their business.

Our partisan duopoly conscripts most Americans into that tug-of-war. Social media makes things worse because airing one's views is inexpensive, even cheaper than voting. Those who neither argue nor vote might be blissfully ignorant, but they are just as powerless. Everyone lives with the acrimony around them and waits for whatever changes are to be handed down by sociopaths in Washington. Such a system creates enmity. (And, indeed, it invites insolvency.)

It’s no wonder.

With the dissolution of the entitlement power apparatus, people will self-organize. They will adopt sweet talk to gain more market share for their organizations as they compete for members. Agitation and anger will dissipate as people transition in free association into systems of mutuality and community.

None of this is to say that conflict will go away entirely. People are people. It means that people will have far stronger incentives to go local, be kind to each other, honor their word, and generally do the right thing when they become active participants in a benefit association instead of wards of the state.